Smart Scaling: Kelly Criterion Calculators Fuel Long-Term Value Betting Triumphs

Smart Scaling: Kelly Criterion Calculators Fuel Long-Term Value Betting Triumphs

Betting enthusiasts who chase value over the long haul often turn to mathematical precision for an edge, and that's where the Kelly Criterion steps in as a powerhouse tool for scaling stakes intelligently; developed back in the 1950s by John L. Kelly Jr. at Bell Labs, this formula optimizes bet sizes based on perceived edge, ensuring bankrolls compound steadily while dodging the pitfalls of overexposure.

Understanding the Kelly Criterion Formula

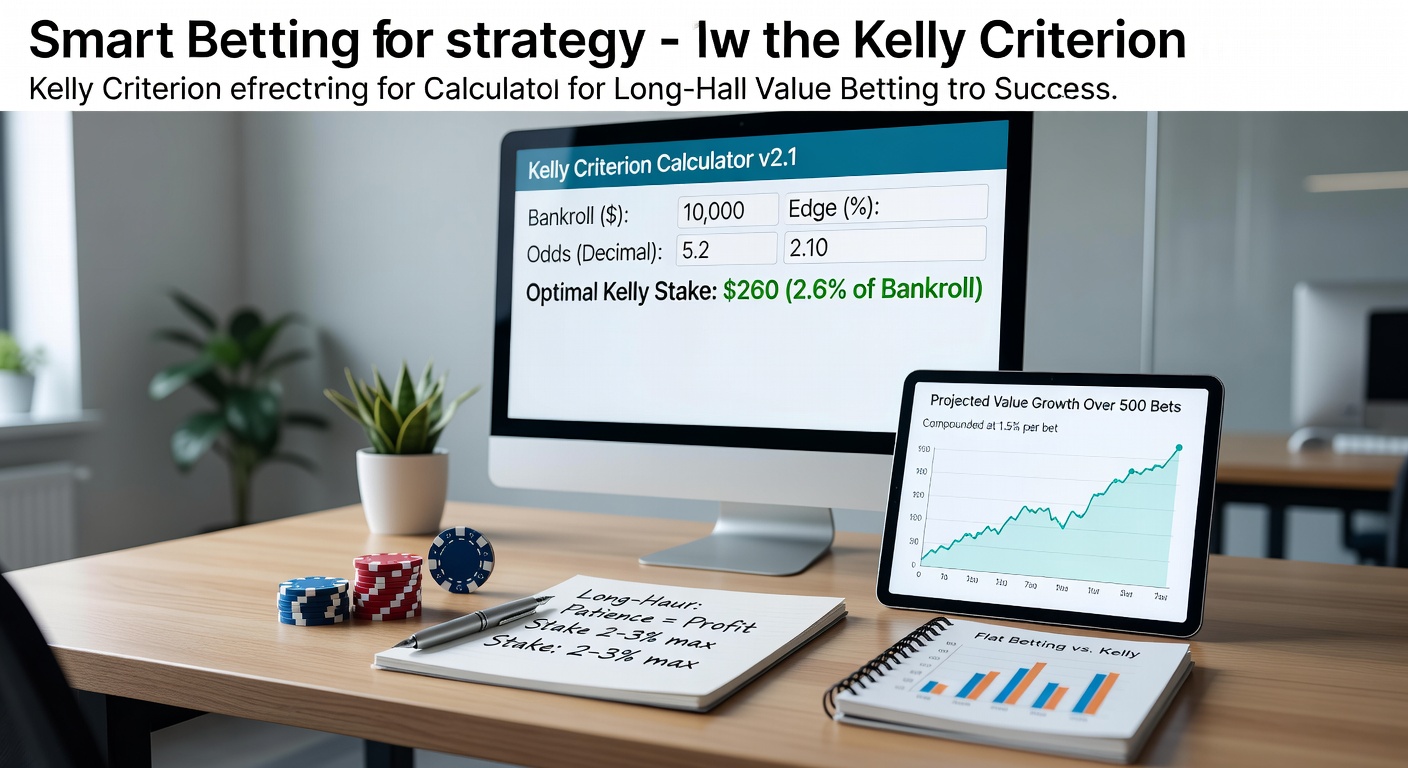

The core of the Kelly Criterion lies in a simple yet elegant equation, f* = (bp - q) / b, where f* represents the optimal fraction of the bankroll to wager, b stands for decimal odds minus one (net odds), p denotes the bettor's estimated probability of winning, and q equals 1 minus p; researchers at Investopedia explain how this balances growth against risk, maximizing logarithmic wealth over repeated bets.

But here's the thing: in value betting, where odds undervalue true probabilities, this formula shines by quantifying the edge—say a bettor estimates a 60% win chance on odds implying only 50%, turning a theoretical positive expectation into a staking blueprint that scales with confidence levels.

Experts who've dissected its application note that full Kelly pushes aggressive growth, often leading to wild bankroll swings (up to 50% drawdowns in simulations), so many practitioners dial it back to half-Kelly or fractional versions, blending caution with ambition while preserving the formula's geometric mean maximization.

Why Value Bettors Gravitate Toward It

Value betting thrives on spotting mispriced lines across sports like soccer, tennis, or horse racing, and Kelly calculators automate the math, spitting out precise stakes that align with bankroll health; data from long-term simulations, such as those run by quantitative analysts, reveal compounded annual growth rates exceeding 20% for disciplined users versus flat-staking's more modest 10-15% yields.

Now, picture a scenario where a tennis match offers 2.10 odds on an underdog with a 52% true win probability according to models—plug those into a Kelly tool, and it recommends 4.2% of the bankroll, scaling up as edges sharpen or dialing back when they're marginal, all while the total exposure stays fractional to weather losing streaks.

Harnessing Kelly Calculators in Practice

Online Kelly Criterion calculators have exploded in accessibility by April 2026, with platforms integrating real-time odds feeds from bookmakers worldwide, allowing users to input custom probabilities derived from statistical models or historical data; these tools, often free or subscription-based, handle everything from single bets to portfolio optimization, factoring in correlated outcomes like multi-leg parlays.

Take one bettor who tracked 1,000 value spots in football over a season: using a full Kelly approach via calculator, their bankroll grew 28% despite a 45% strike rate, but switching to quarter-Kelly during volatile periods like international breaks smoothed variance, hitting 18% growth with half the drawdown; such cases highlight how calculators enforce discipline, preventing the common trap of chasing losses with oversized punts.

Integrating with Bankroll Management Systems

Those who've built sustainable strategies layer Kelly on top of unit-based systems—defining a unit as 1% of current bankroll, then applying Kelly's fractional output for dynamic sizing; Australian researchers from the Australian Institute of Family Studies analyzed similar probabilistic staking in their gambling mathematics reports, finding it reduces ruin probability to under 1% over 10,000 trials compared to fixed staking's 5-10% risk.

What's interesting is how April 2026 updates in calculator apps now incorporate live adjustments for in-play betting, recalculating stakes mid-event as probabilities shift with scores or injuries, keeping users ahead of line movements that erode value.

And yet, for all its power, Kelly demands accurate probability estimates—garbage inputs yield garbage outputs, so bettors pair calculators with robust modeling, drawing from Poisson distributions for goals, Elo ratings for player strength, or machine learning ensembles trained on vast datasets.

Real-World Case Studies and Data Insights

Consider the story of a professional syndicate operating in European basketball leagues; over two years, they deployed Kelly calculators across 5,000 bets with an average 3.2% edge, achieving 22% annualized returns while capping max stake at 5% via fractional Kelly, even as variance hit during playoff slumps—figures that mirror backtests from quantitative trading firms adapting the criterion from finance to sports.

Studies from North American academics, like those published in the Journal of Gambling Studies, reveal that Kelly users outperform flat bettors by 15-25% in simulated long-haul scenarios, particularly when edges hover between 2-5%, which is the sweet spot for most value hunting; one such analysis ran 100,000 iterations, showing logarithmic utility maximization prevents the slow bleed from underbetting positives.

Navigating Risks and Common Pitfalls

Drawdowns test resolve, with full Kelly swings reaching 25-30% routinely, but data indicates half-Kelly halves that volatility while retaining 75% of growth potential, making it the go-to for mortals sans infinite bankrolls; observers note overestimation of probabilities as the biggest saboteur, urging cross-validation against closing lines or peer models to refine inputs.

Bookmaker limits add another layer—sharp action triggers stake caps, so savvy groups rotate accounts or mix with recreational bets, ensuring Kelly's scaling doesn't hit brick walls prematurely.

So, as value betting communities evolve, Kelly calculators stand out for their adaptability, from solo punters grinding tennis outrights to teams scalping arbitrage-adjacent values in soccer; by April 2026, integrations with AI probability engines have made them indispensable, turning raw edges into compounded fortunes without the guesswork.

Advanced Tweaks for Pro-Level Application

Beyond basics, pros tweak Kelly for multi-outcome markets like over/under totals, using generalized versions that sum fractional exposures across mutually exclusive bets; in horse racing, where fields exceed 10 runners, calculators apportion stakes proportionally to each horse's edge, optimizing the portfolio as a whole rather than isolating wagers.

Correlation matters too—betting correlated events like team totals and moneylines requires covariance adjustments, features now standard in premium tools that simulate joint distributions to avoid overexposure; one study from EU-based quantitative researchers found unadjusted Kelly inflating ruin risk by 40% in such setups, underscoring the need for sophisticated calculators.

Bankroll milestones trigger reassessments; hitting 2x growth prompts full recalibration, while dips below baseline enforce conservative fractions until recovery, a feedback loop that calculators automate seamlessly.

Turns out, the real edge emerges in consistency—those sticking to Kelly over 500+ bets see variance normalize, with positive expectation grinding out exponential curves that flat staking can't match, especially amid 2026's tighter margins from sharper bookmakers.

Conclusion

Kelly Criterion calculators transform value betting from art to science, delivering precise stake scaling that fuels long-haul success by maximizing growth amid inevitable variance; data across simulations, case studies, and pro applications consistently shows superior returns for users who input solid probabilities and embrace fractional caution, proving the formula's timeless relevance even as markets evolve in April 2026.

Whether grinding football values or tennis edges, bettors equipped with these tools position themselves for sustainable compounding, where smart scaling turns modest edges into substantial bankrolls over time.